ASCs vs HOPDs: When performing outpatient procedures, many orthopedic surgeons operate in ASCs or hospital-based outpatient departments (HOPDs). Although some of the workflows and services offered may appear similar between the two, the background operations are substantially different from a business and regulatory perspective.

An HOPD is owned by and typically attached to a hospital, whereas an ASC is considered a standalone facility. This study aimed to compare the utilization and cost of ASCs vs HOPDs.

The difference between an ASC and an HOPD concerns the regulations that apply to the center; therefore, a “freestanding” surgery center can still be classified as an HOPD if it is within a 35-mile radius of a hospital and is under the same financial and administrative contracts.

Similarly, a hospital can operate a facility and still maintain ASC status if it is a financially and administratively independent entity with its own Medicare agreement. Furthermore, ASCs must comply with the ASC Covered Procedures List, which ensures that procedures with the appropriate level of risk are performed in these freestanding centers.

Payment Overview and Research

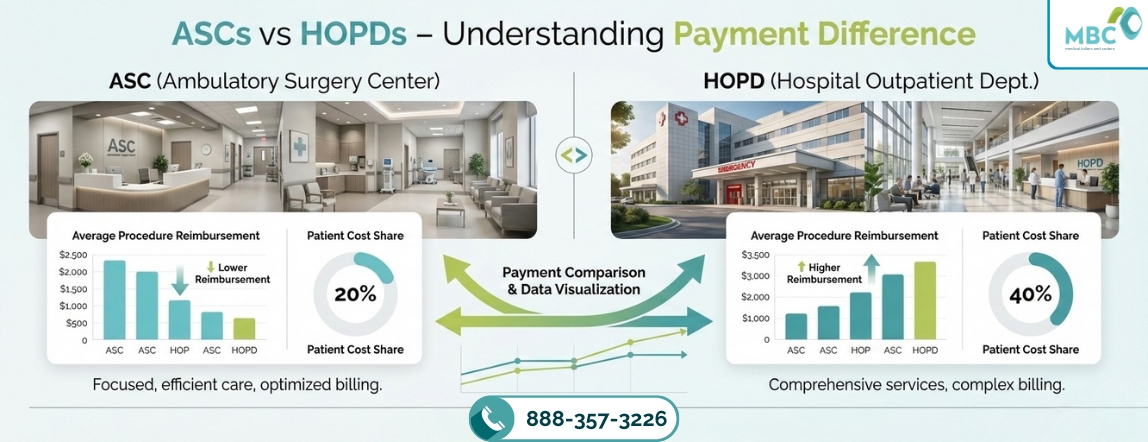

In general, ASCs command lower rates than their HOPD counterparts. Using Medicare as an example, when outpatient surgeries shift from an HOPD setting to a freestanding ASC, the Medicare payment methodology changes from the Outpatient Prospective Payment System (OPPS) to the ASC fee schedule.

This shift is impactful because although the ASC fee schedule is linked to OPPS payments, the inputs and adjustments to the calculation differ.

Medicare rates, a diagnostic colonoscopy (CPT® code 45378) would have an allowable payment rate of $709.98 in an HOPD setting, while the same procedure would have an allowable payment rate of $369.84 in a freestanding ASC (about 52 percent of the HOPD rate).

Differences in Methodology Lead to Different Payments of ASCs vs HOPDs

Three main factors contribute to the differences in payment between ASCs vs HOPDs

1. Relative weight:

The relative weight is the numerical value associated with the service provided, as defined by the Centers for Medicare & Medicaid Services (CMS). This value is multiplied by the conversion factor to determine the national Medicare allowable rate.

The relative weight is lower in the freestanding ASC setting due to OPPS’s proportional adjustments to relative weight to maintain budget neutrality. This methodology resulted in a 10.1 percent reduction in the ASC relative weight (when compared with the HOPD relative weight) for 2018.

2. Conversion factor:

The ASC conversion factor is now based on the hospital market basket, whereas previously, it was based on the Consumer Price Index. The change to the hospital market basket promotes site neutrality between hospitals and ASCs and encourages the migration of services from the hospital setting to the lower-cost ASC setting.

Thus, the ASC conversation factor is $46.55 for 2019, and the OPPS conversion factor, also based on the hospital market basket, is $79.49 for 2019. As such, the ASC conversion factor is about 59 percent of the OPPS conversion factor ($46.55 / $79.49 = 59 percent).

3. Wage index adjustment:

Once the national Medicare allowable rate (allowable rate) is determined, it is further adjusted by the geographical wage index of each individual HOPD/ASC. The geographical wage index for each HOPD/ASC is determined by calculating the ratio of the average hourly wage for its labor market (typically its county) to the national average hourly wage.

This geographical wage index adjustment varies for HOPD payments and freestanding ASC payments.

For freestanding ASCs, the 50 percent of the allowable rate is adjusted. For HOPDs, the 60 percent of the allowable rate is adjusted. This difference in methodology and weighting (as it relates to the labor portion of the payment) can positively or negatively impact ASC payment rates when compared with the OPPS rates, depending on the applied wage index.

Total Costs for Four Eye Procedures

The total cost is the “Medicare-approved amount.” In Original Medicare, Medicare generally pays 80 percent of this amount, and the patient pays 20 percent.

66984: Extracapsular cataract removal with insertion of intraocular lens prosthesis, a one-stage procedure

- ASC: $977

- HOPD: $1,917

67028: Injection of the drug into the eye

- ASC: $48

- HOPD: $288

66821: Removal of recurring cataract in lens capsule using laser

- ASC: $255

- HOPD: $496

66982: Extracapsular cataract removal with insertion of intraocular lens prosthesis, complex

- ASC: $977

- HOPD: $1,917

As a result of the transitions, solutions such as comanagement agreements have been developed to allow physicians to exercise some leadership in managing HOPDs without the financial risks associated with ASC ownership.

Current efforts to equalize payments between ASCs and HOPDs, along with the addition of several key procedures to the ASC Covered Procedures List, are likely to impact the ASC and HOPD markets. The changes, along with a shift toward value-based care, will play important roles in the future of systems that support outpatient orthopedic procedures.

Medical Billers and Coders (MBC) is one of the leading medical billing service providers. With 15+ years of experience in medical billing and proven services, many surgical centers across the country have overcome denials and underpayments.

Our billing professionals not only specialize in coding and billing but also incorporate the knowledge throughout the process. To know more about our Ambulatory Surgical Centers Medical Billing Services, you can contact us at 888-357-3226 / info@medicalbillersandcoders.com

Reference:

HOPDs vs. ASCs: understanding payment differences

FAQs:

An ASC is a standalone facility, while an HOPD is part of a hospital, though both can offer similar services.

ASCs generally receive lower payment rates than HOPDs for the same procedures due to different payment methodologies.

Key factors include relative weight, conversion factor, and wage index adjustment.

The ASC conversion factor is lower, about 59% of the HOPD factor, impacting the overall payment amount.

Comanagement agreements allow physicians to lead HOPDs while minimizing financial risks compared to owning ASCs.

With almost 12 years of experience in healthcare revenue cycle management, this Revenue Cycle Specialist brings deep expertise in medical billing, claims optimization, and practice profitability. Shares industry-backed insights focused on improving collections, reducing denials, and driving operational excellence.